THE AUTHOR:

Tiffany Lam, Strategic Communications & AI Ethics Officer at Jus Mundi

In 2025, institutional caseloads approached near-record highs whilst dispute values surged. The International Court of Arbitration of the International Chamber of Commerce (“ICC”) reported USD 299 billion in pending disputes by year-end 2025, reflecting continued growth across both volume and value dimensions.

Based on newly published annual statistics from leading arbitration institutions worldwide, including the ICC, Singapore International Arbitration Centre (“SIAC”), Hong Kong International Arbitration Centre (“HKIAC”), London Court of International Arbitration (“LCIA”), China International Economic and Trade Arbitration Commission (“CIETAC”), American Arbitration Association-International Centre for Dispute Resolution (AAA-ICDR), Stockholm Chamber of Commerce Arbitration Institute (“SCC”), and International Centre for Settlement of Investment Disputes (“ICSID”), six interconnected insights emerge that signal where the market is heading.

Trend 1: Geographic Shifts Reshape the Arbitration Market

Traditional arbitration hubs including Paris, London, and New York remain powerful centres of practice. However, the 2024-2025 data demonstrates that the global picture is becoming markedly more balanced, with Asia-Pacific, Latin America, Africa, and the Middle East rapidly gaining institutional credibility and market share.

The rise of Asian seats represents the clearest evidence that arbitration’s geographic centre of gravity is shifting. Singapore and Hong Kong tied with London at 31–34% as preferred arbitral seats globally, according to the 2025 Queen Mary University of London and White & Case International Arbitration Survey (2025 International Arbitration Survey). This preference reflects substantial institutional growth. In Singapore, not only did SIAC’s caseload grow 227% from 2015 to 2025 (271 cases to 886 cases), an integrated dispute resolution ecosystem has also been constructed to complete the offering to arbitration users. Hong Kong, meanwhile, offers a distinct strategic advantage as an enforcement bridge with Mainland China. HKIAC processed 34 applications worth USD 1.6 billion in 2025 under the Mainland China Interim Measures Arrangement, while it received a total of 388 new cases (a 10.2% growth from 2024). Additionally, HKIAC has positioned itself as a leading venue for digital asset disputes, with cryptocurrency and blockchain cases accounting for 7.2% of its 2025 arbitrations.

Latin America demonstrates sustained momentum. One-third of ICSID investment arbitration cases in 2025 involved Latin American states, and regional seats including São Paulo, Santiago, and Mexico City are increasingly chosen over traditional European or American venues, reflecting both the region’s economic significance and deliberate support for local dispute resolution infrastructure.

In Africa, states are updating arbitration laws, strengthening recognition and enforcement frameworks in alignment with the New York Convention (1958), and building regional hubs in jurisdictions including Mauritius, Rwanda, Nigeria, and South Africa.

The Middle East, particularly the Gulf region, is undertaking an aggressive institutional build-out backed by substantial government investment. The United Arab Emirates entered ICC’s top five arbitration seats in 2024, while the Saudi Centre for Commercial Arbitration achieved 65% average annual caseload growth over the past four years — a significant sustained growth rate of any major arbitral institution worldwide, reaching 120 cases and USD 304 million in disputes in 2024. New institutions have also emerged across the region, including the Bahrain International Commercial Court and arbitrateAD in Abu Dhabi, signalling coordinated efforts to establish Gulf jurisdictions as credible arbitration centres.

Trend 2: Institutions Compete on Efficiency

As arbitration centres proliferate globally, institutions face intensified competition for caseload. Efficiency has emerged as a central differentiator, with parties increasingly expecting demonstrable value in terms of both speed and cost.

Routine, lower-value disputes are increasingly channelled into faster, lower-cost procedural tracks with compressed timelines (typically 3 to 6 months to award) and simplified rules. In this context, expedited procedures have gained significant traction across institutions. At ICC, nearly one in five cases (169 out of 894) proceeded under Expedited Procedure Provisions in 2025, representing an 11.2% increase from 2024. At SIAC, one in eight cases in 2025 utilised either the Expedited Procedure (which crossed its 1,000th application milestone in 2024) or the newly introduced Streamlined Procedure, a further simplified track for lower-value disputes that processed 60 cases in its inaugural year.

Cost optimisation extends beyond track selection. At the American Arbitration Association-International Centre for Dispute Resolution, 49% of settled cases in 2025 closed before incurring any arbitrator compensation, reflecting early settlement facilitation. Furthermore, for high-value disputes exceeding USD 3 million, parties who opted for a sole arbitrator rather than a three-member tribunal saved 83% in arbitrator compensation — a choice made in over 50% of such cases.

Legislative reforms are reinforcing this drive toward procedural efficiency*.* England’s Arbitration Act 2025, which came into effect in August 2025, introduced summary disposal mechanisms for unmeritorious claims and codified courts’ supportive role in arbitration, expected to reduce costs and delays further in London-seated arbitrations. For a comprehensive analysis of global legislative developments, see Jus Mundi’s 2025 Arbitration Year in Review.

Institutions that cannot demonstrate measurable value on speed and cost risk losing competitiveness to more efficient alternatives, driving continuous procedural innovation and making efficiency metrics increasingly transparent and comparable.

Trend 3: Sectors Diversify as New Dispute Types Emerge

The sectoral composition of arbitration caseloads reveals both continuity and transformation. Traditional dispute drivers remain robust, whilst categories such as technology disputes and energy transition claims are reshaping the market’s sectoral mix.

Construction and energy continue to form the core of institutional caseloads globally. Combined, these sectors represented 44% of ICC’s 2024 caseload; oil, gas, and mining accounted for 43% of ICSID investment cases in 2025, with construction representing a further 15% and electric power and other energy 12%; at Dubai International Arbitration Centre (“DIAC”), construction and real estate dominated approximately 60% of the 2024 caseload. Large-scale infrastructure projects and natural resource extraction continue to generate the complex, high-value disputes that have historically sustained arbitration practice.

The American market reveals a different sectoral composition. At AAA-ICDR, technology disputes represented the largest category with 150 cases in 2025, outpacing construction, financial services, and energy.

Notably, technology disputes are increasingly embedded within traditional sectors rather than remaining siloed. Within technology disputes, artificial intelligence (“AI”)-related claims are expected to emerge as a rapidly growing subcategory. These disputes include data ownership, intellectual property over AI-generated content, algorithmic liability, and data breach responsibility. Baker McKenzie’s 2025 Disputes Survey of 600 senior in-house lawyers found that 44% cite AI-related disputes as a significant risk over the next five years, with primary concerns including data privacy and security, ethical issues around AI decision-making, and intellectual property infringement involving AI-generated outputs. Arbitration’s distinguishing features — confidentiality, access to arbitrators with specialised expertise, and procedural flexibility — make it particularly well-suited to technology disputes where proprietary information and technical complexity are central.

Together, sectoral diversification and technical complexity are driving demand for domain-specific expertise and sophisticated research capabilities.

Trend 4: AI Transforms Both Practice and Procedure

Perhaps no force in the arbitration market is accelerating faster than AI adoption, which is transforming both how practitioners conduct their work and how institutions administer proceedings. The speed and scale of this transformation, evidenced by recent survey data and institutional innovations, suggest that AI integration will become a defining feature of arbitration practice within the current decade.

The adoption trajectory is steep. The 2025 International Arbitration Survey found that 64% of practitioners currently use AI for legal research; with 91% expecting to do so within five years. For drafting submissions, current usage stands at 28%, but 66% expect to rely on AI for this purpose within five years. Additionally, 52% of respondents expect arbitrators themselves to increasingly rely on AI tools in their decision-making processes.

Institutions are moving from pilot programmes to operational reality. In November 2025, AAA-ICDR launched the first AI Arbitrator for certain construction cases (subject to a set of requirements), where AI drafts a proposed outcome that is subsequently reviewed and authorised by human arbitrators. By March 2026, AAA-ICDR had expanded this initiative with a Resolution Simulator tool, allowing practitioners to test dispute scenarios and receive simulated non-binding outcomes before filing, thereby informing negotiation strategy, settlement positioning, and client advice. This aligns strategically with AAA-ICDR’s user demographics: as noted previously, technology is by far the institution’s largest sectoral category, creating natural incentives to pioneer technology-forward procedural rules that appeal to tech-sector users.

Leading institutions and judiciaries are issuing AI usage protocols and guidelines, shaping how AI is integrated into arbitration practice. For practitioners navigating this evolving landscape, the JM AI Hub offers a carefully curated collection of foundational and emerging legal resources that address AI in legal practice and dispute resolution. As this guidance matures, AI literacy and adoption are transitioning from optional enhancement to essential capability.

Trend 5: Geopolitical Fragmentation Fuels the Dispute Pipeline

As geopolitics shape what disputes enter the arbitration pipeline, three vectors are creating sustained demand for cross-border dispute resolution services.

Tariff-related commercial disputes represent the first vector. United States tariffs reached 100-year highs in 2025, straining existing commercial relationships. As contracts face delayed performance, increased costs, and questions of commercial impracticability, the volume of tariff-related disputes is expected to grow.

Sanctions-related claims form the second vector. At least 28 sanctions-related investor-state disputes worth approximately USD 62 billion have been filed by Russian investors following sanctions imposed after the Ukraine conflict, with more than half filed in 2025 alone. As a consequence, seat selection — always a strategic consideration — has taken on heightened significance: according to the 2025 International Arbitration Survey, 30% of practitioners who experienced sanctions-related complications in their cases chose a different arbitral seat to safeguard enforceability of any eventual award, with Dubai, Hong Kong, and Singapore emerging as preferred safe harbour jurisdictions.

Armed conflict zones constitute the third vector. Investment arbitration remains particularly active in conflict-affected regions: ICSID administered a record 347 cases in fiscal year 2025, with Sub-Saharan Africa, Central America and the Caribbean, and South America leading respondent regions. Many of these involve disputes arising from political instability, regulatory changes, or state measures taken in response to security concerns.

Trend 6: Diversity Progress Remains Uneven

Gender diversity in arbitrator appointments continues to improve incrementally, but progress remains slow and reveals a persistent structural gap between institutional appointments and party nominations.

Across major institutions, female arbitrator appointments in 2024–2025 ranged from 28% to 37% of total appointments. However, the critical distinction lies in who makes the appointment: when institutions directly appoint arbitrators, women represent 35 to 46% of appointments; where parties nominate arbitrators, women represent only 17 to 24% of nominations. This gap is consistent across institutions and represents a structural challenge.

The Diversity Gap: Data Across Institutions

| Institution | Overall Women % | Institutional Appointments | Party Nominations | Gap |

|---|---|---|---|---|

| ICC (2024) | 28.6% | 46% | 19% | 27 points |

| LCIA (2024) | 33% | 45% | 21% | 24 points |

| SIAC (2024) | / | 35% | / | / |

| VIAC (2024) | 37% | 64% | 17% | 47 points |

| HKIAC (2025) | / | 36.4% | 24.1% | 12.3 points |

The data reveals that sustained progress requires further participation from parties and counsel, alongside institutional efforts.

What the Patterns Reveal

The 2024-2025 institutional caseload data, taken collectively, reveals the maturation of a globalising market undergoing simultaneous consolidation and transformation. The market is consolidating its position as the dominant mechanism for high-value cross-border disputes. At the same time, it is transforming geographically, sectorally, technologically, procedurally, and structurally.

These six trends are interconnected. Geographic expansion drives institutional competition on efficiency. Technology sector growth drives AI adoption in practice. Geopolitical fragmentation reinforces the value proposition of neutral arbitration venues. Sectoral diversification creates demand for specialised expertise and sophisticated research tools. Each trend reinforces the others, creating momentum toward a more global, efficient, technologically sophisticated, and geopolitically responsive arbitration market.

Practitioners and institutions that understand these patterns and position their practices and procedures accordingly will be best placed to succeed in an increasingly competitive and rapidly evolving market.

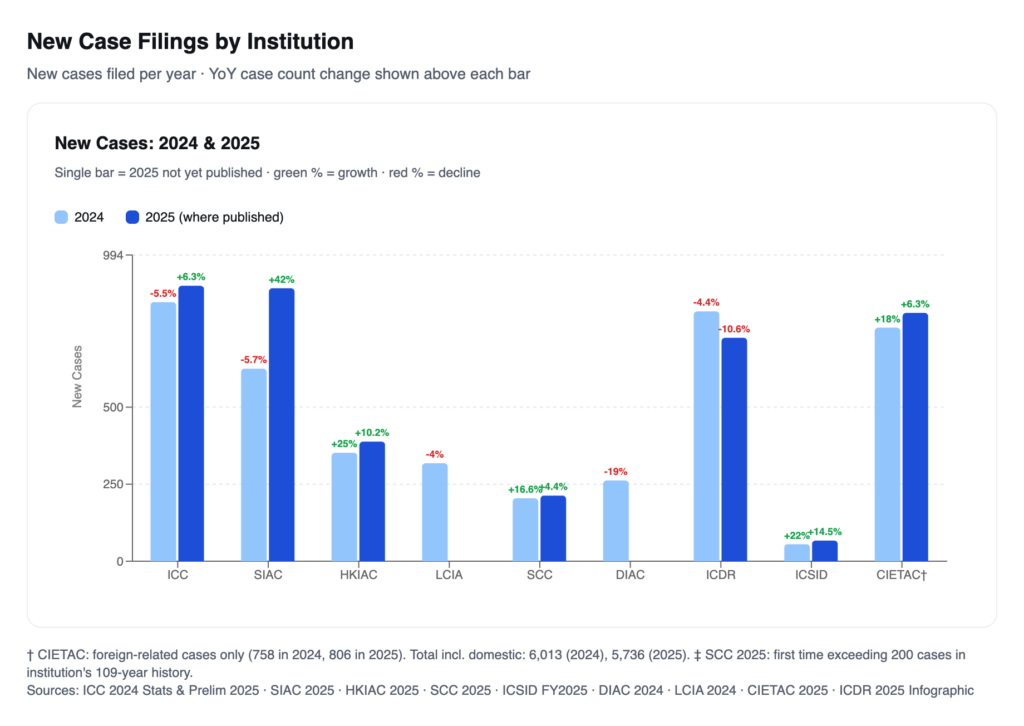

Key Statistics at a Glance

Data Table

| Institution | 2024 New Cases | YoY Change (vs 2023) | 2025 New Cases | YoY Change (vs 2024) |

|---|---|---|---|---|

| ICC | 841 | -5.5% | 894 (prelim.) | ↑ +6.3% |

| SIAC | 625 | -5.7% | 886 (2nd highest year) | ↑ +42% |

| HKIAC | 352 | +25% | 388 | ↑ +10.2% |

| LCIA | 318 | -4% | Not yet published | — |

| SCC | 204 | +16.6% (2nd highest year) | 213 | +4.4% |

| DIAC | 262 | -19% | Not yet published | — |

| ICSID | 55 | +22% | 67 | ↑ +14.5% |

| CIETAC | 6,013 | +14.8% | 5,736 | -4.6% |

| – CIETAC, Foreign-related | 758 | +18% | 806 | ↑ +6.3% |

| ICDR | 811 | 725 | -10.6% |

Methodology Note

This analysis is based on published annual statistics from institutional arbitration centres, including ICC, SIAC, HKIAC, ICSID, LCIA, SCC, DIAC, Vienna International Arbitral Centre (VIAC), CIETAC, and AAA-ICDR, covering 2024 and (where available) 2025.

Institutions may define their data points differently, limiting perfect comparability across institutions. Data reported reflects either published final statistics, preliminary figures or, where 2025 data remains unpublished as of March 2026, the most recent available year.

A more detailed analysis of global legislative developments are available in Jus Mundi’s 2025 Arbitration Year in Review.

About Jus Mundi

Founded in 2019 and recognized as a mission-led company, Jus Mundi is a pioneer in the legal technology industry dedicated to powering global justice through artificial intelligence. Headquartered in Paris, with additional offices in New York, London, and Singapore. Jus Mundi serves over 150,000 users from law firms, multinational corporations, governmental bodies, and academic institutions in more than 80 countries. Through its proprietary AI technology, Jus Mundi provides global legal intelligence, data-driven arbitration professional selection, and business development services.

*The views and opinions expressed by authors are theirs and do not necessarily reflect those of their organizations, employers, or Daily Jus, Jus Mundi, or Jus Connect.